Mortgage Guide

Why is my first mortgage payment higher?

If you weren’t expecting it, your first mortgage payment can feel like a nasty shock.

If the amount is higher than you were expecting, it’s understandable to worry that something’s gone wrong.

In reality, this is very common — and for most people, payments return to the expected amount from month two.

Quick takeaways

- Your first mortgage payment often covers more than one month.

- It usually includes daily interest from the date you complete.

- It will usually revert to your expected amount from the second payment onwards.

- A higher first payment is normal — not a sign something’s gone wrong.

Understanding your first mortgage payment

When you complete your mortgage, your lender starts charging you interest straight away — from the day you collect your keys. But your regular direct debit date (say the 1st of the month) might not line up neatly with that completion date.

The most common way a lender handles this is by adding that “in-between” interest to your first mortgage payment. So your first payment will typically include:

- Daily interest from completion to your first payment date

- Your first full month’s mortgage payment

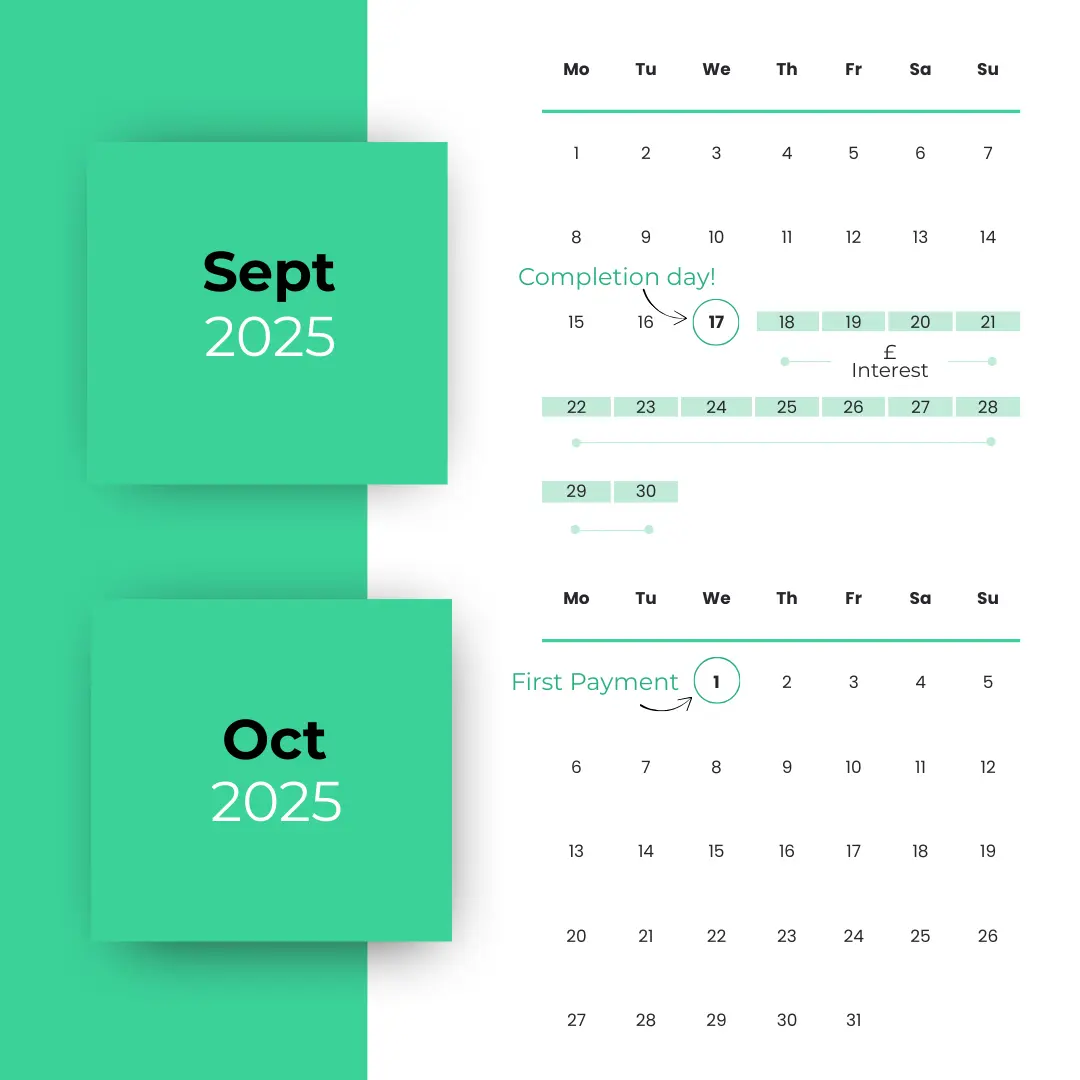

Example

A typical timelineLet’s say you complete on 17th September and agree to pay your mortgage on the 1st of each month.

Why do lenders do this?

It’s all about interest accuracy. Lenders need to collect interest for every day you owe them money. By adding the daily interest into the first payment, they avoid undercharging and then having to recalculate later.

Budgeting for your first mortgage payment

A higher first mortgage payment can feel like a bit of a shock if you’re not expecting it. The good news? With a little planning, you can take it in your stride.

Estimate the cost ahead of time

Ask your broker or lender to calculate the likely first payment before you complete. That way, you won’t get caught off guard when your first direct debit leaves your account.

Keep a buffer fund

It’s smart to keep at least 1.5× your expected monthly mortgage payment in a separate account during the first month. This gives you breathing space for the extra daily interest.

Adjust other commitments

If possible, keep other big expenses away from that first month. It may mean delaying that TV and sofa purchase… but future you will thank you (even if from the temporary beanbag).

Revisit your budget after the first payment

Once the first payment is done and you’ve seen your regular monthly amount in action, it’s a great time to review your budget to make sure you stay on track.

Want the full first-time buyer checklist?

Download our free First-Time Buyer Guide for a smoother journey onto the property ladder.

FAQs

Your first mortgage payment often includes daily interest from your completion date to the end of that month, as well as your first full monthly payment.

In most cases, yes. The amount depends on when you complete in the month and when your direct debit is set. After your first payment, your mortgage usually settles into your regular monthly amount.

Some lenders let you choose your preferred payment date, but you’ll still need to cover the daily interest from completion to that point. Ask for a breakdown before completion if you're concerned.

Need a hand?

We can run through your scenario, your numbers and your options — and get you feeling clear and confident.

What our clients say about us ✪✪✪✪✪

We’re proud to help homeowners, buyers, and investors across Broadstairs, Kent and beyond with expert mortgage and financial advice. See what our happy clients have to say!

THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR HOME.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE OR ANY OTHER DEBT SECURED ON IT.

IMPORTANT: With investments, your capital is at risk. Pensions and investments can go down in value as well as up, so you could get back less than you invest.

Need Financial Planning Ltd is registered in England and Wales no. 10901658. Registered office, 123 High Street, Broadstairs, Kent, CT10 1NQ. Authorised and regulated by the Financial Conduct Authority. Need Financial Planning Ltd is entered on the Financial Services Register https://register.fca.org.uk/ under reference 977136. If you wish to register a complaint, please write to [email protected] or telephone 01843 228800. A summary of our internal complaints handling procedures for the reasonable and prompt handling of complaints is available on request and if you cannot settle your complaint with us, you may be entitled to refer it to the Financial Ombudsman Service at www.financial-ombudsman.org.uk or by contacting them on 0800 0234 567.

© Copyright 2022 Need Financial Planning Ltd. All rights reserved. Privacy Policy | Disclaimer | Cookie Policy