Is my current deal still competitive?

We’ll compare your lender’s offers with the wider market so you can see if a simple switch or a full remortgage makes more sense.

Whether your fixed rate is ending, you’re worried about rising payments, or you’d like to borrow more for home improvements, we’ll walk you through your choices in plain English. We’ll compare staying with your current lender versus switching, explain the pros and cons, and help you move onto a mortgage that actually fits where you are now.

Most people we speak to feel uneasy about remortgaging: “Will my payments shoot up?”, “Do I have to stay with my current lender?”, “Can I borrow more without over-stretching?”.

Our job is to take the guesswork out of it. We’ll review your current mortgage, explain your options in plain English, and show you the numbers side by side – so you can make a calm, informed choice instead of feeling rushed or confused.

We’ll compare your lender’s offers with the wider market so you can see if a simple switch or a full remortgage makes more sense.

We’ll model different rates, terms and options so you can see how your payments might change and what feels comfortable.

Whether it’s for home improvements, debt consolidation or another goal, we’ll show you how much you could borrow – and the long-term impact.

New job, self-employed, maternity leave or credit blips – we’ll talk through how lenders may view things and which options are realistic.

From first questions to your new deal going live, here’s how we guide you through. You’ll always know what’s happening, why it’s happening, and what we’re doing in the background.

We’ll start with a relaxed conversation to understand your current mortgage, when your deal ends, and what you’d like your remortgage to achieve - whether that’s lower payments, more certainty or raising funds.

You’ll complete a secure fact-find and upload your documents so we can properly review your current position and prepare everything accurately from the start.

Using your fact-find and documents, we’ll walk you through the options available and what your new mortgage could look like. We’ll also discuss your preferences, such as budget, change to term length and whether to raise additional funds, to help shape the right direction.

Where needed, we carry out initial lender checks and secure a Decision in Principle to give an early indication of how a lender is likely to view your application.

Once we’ve refined everything based on your preferences and circumstances, we’ll recommend the most suitable mortgage for you and explain exactly why it fits.

We submit your full application and manage the process with the lender, keeping everything moving and handling any queries through to your mortgage offer.

Once the offer is issued, any legal work is completed in the background. For many simple remortgages this is very straightforward – we’ll explain exactly what’s needed in your case.

Your new deal replaces your old one, your payments switch over and we’ll confirm everything in writing. We’ll also talk about future reviews so you’re not left drifting onto a high variable rate again.

Prefer to play with the numbers first? These free tools give you a feel for how different rates, terms and overpayments might look before we talk things through properly.

Not sure what to expect? These FAQs explain how our intro call works and how we can help.

If you’re new to us, the intro call is the best place to start. It’s a simple, no-pressure conversation where we’ll talk through your situation, what you’re hoping to achieve, and any questions you might have. From there, we’ll guide you on the best way forward.

You’ll always know who you’re dealing with. Your remortgage advice will be handled by James or Rob, with Lucy and Chrissie keeping everything on track behind the scenes.

James specialises in helping clients see the bigger picture – from your current mortgage deal through to long-term financial planning, pensions and later-life lending.

Rob is calm, clear and detail-focused. He’ll help you understand your remortgage options, weigh up product transfers versus switching lenders, and make sure everything is set up properly – with protection advice to keep you and your loved ones secure.

Lucy keeps your remortgage application moving – chasing updates, coordinating paperwork and making sure you always know what’s happening next.

Chrissie looks after the guides, updates and little touches that make the remortgage process feel clearer and more organised from day one.

We’re proud to have helped first-time buyers, home movers and remortgagers across Broadstairs, Thanet and beyond. Here’s what some of them had to say:

Whether your rate is ending, payments are rising, or you’re thinking about borrowing more, these quick answers will help you understand your options and the timing.

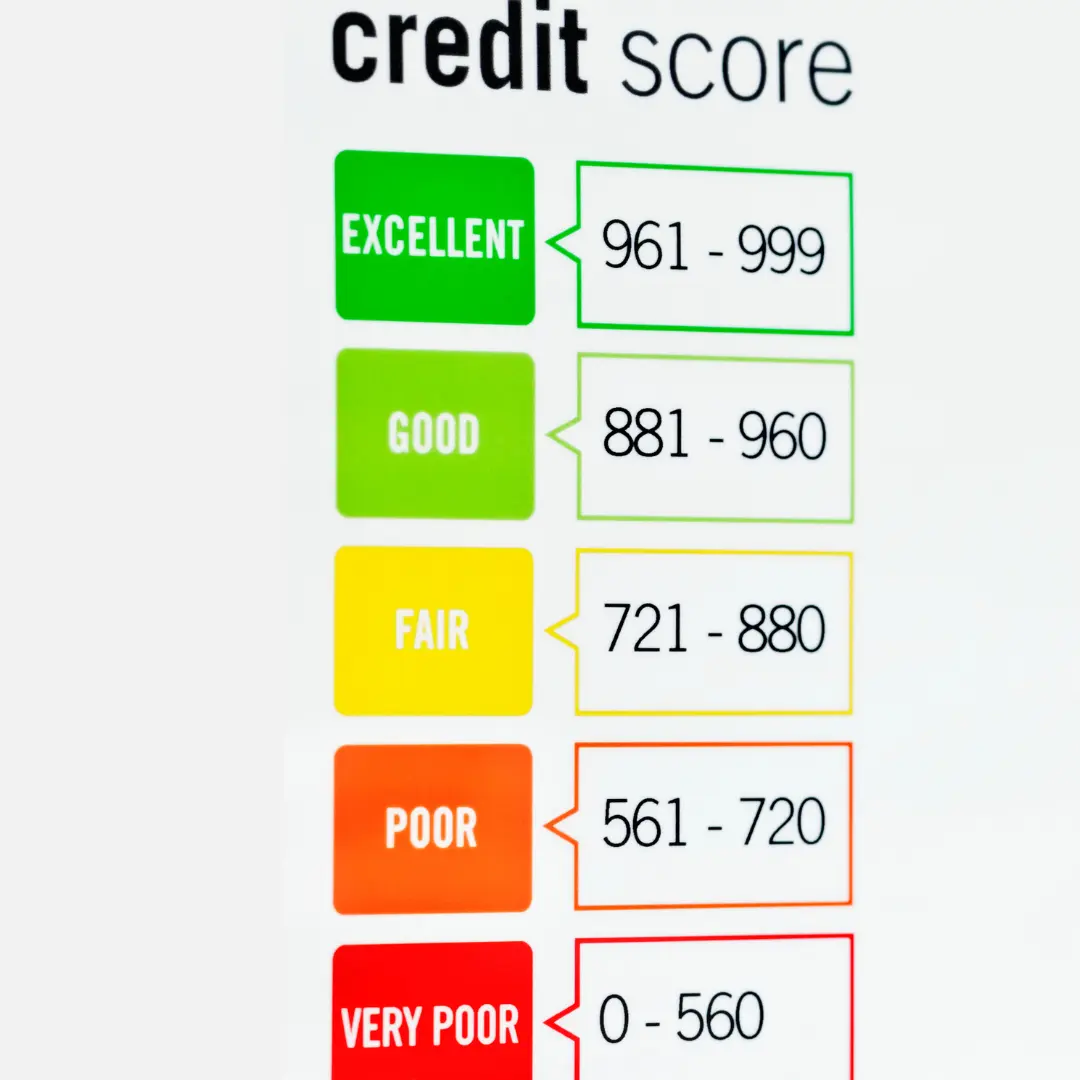

When your fixed rate ends, most lenders move you onto their Standard Variable Rate (SVR). SVRs are often higher (and can change), so it’s usually worth reviewing your options well before the end date.

The key is timing: you want enough breathing space to compare deals, factor in fees, and avoid drifting onto the SVR by default.

It depends. Staying with your current lender (a “product transfer”) can be quicker and may involve less paperwork. Switching lender (a full remortgage) can sometimes save money, but you’ll want to compare the rate and the fees.

We will always compare both routes and recommend what actually makes sense for your situation — not just the headline rate.

Many people start reviewing their options around six months before their deal ends. Some lenders allow applications to be submitted months in advance, which means you can secure a rate and still complete closer to the end date.

We’ll also check any early repayment charges so you don’t switch too soon and accidentally create an unnecessary cost.

Often, yes — subject to affordability and the lender’s criteria. People commonly borrow more for home improvements, consolidating debts, or other “capital raising” reasons.

If you’re increasing the mortgage, we’ll look at the cost of borrowing more, the impact on monthly payments, and whether it’s better to take it as a single loan or a separate “further advance”/additional borrowing.

If you stay with your current lender on a product transfer, you may not need to supply much paperwork. If you switch lender (a full remortgage), it’s common to be asked for updated documents such as payslips, bank statements, and proof of any additional income.

We’ve put the full document checklist together here:

Read more: mortgage application documents

Yes — it’s one of the best times. Your mortgage is a long-term commitment, and remortgaging is a natural checkpoint to make sure your cover still matches your life now (especially if your borrowing is increasing, you’ve had children, or your monthly budget has changed).

If you want a plain-English overview of the main protection options, start here:

Read more: protection overview

THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR HOME.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE OR ANY OTHER DEBT SECURED ON IT.

IMPORTANT: With investments, your capital is at risk. Pensions and investments can go down in value as well as up, so you could get back less than you invest.

Need Financial Planning Ltd is registered in England and Wales no. 10901658. Registered office, 123 High Street, Broadstairs, Kent, CT10 1NQ. Authorised and regulated by the Financial Conduct Authority. Need Financial Planning Ltd is entered on the Financial Services Register https://register.fca.org.uk/ under reference 977136. If you wish to register a complaint, please write to [email protected] or telephone 01843 228800. A summary of our internal complaints handling procedures for the reasonable and prompt handling of complaints is available on request and if you cannot settle your complaint with us, you may be entitled to refer it to the Financial Ombudsman Service at www.financial-ombudsman.org.uk or by contacting them on 0800 0234 567.

© Copyright 2022 Need Financial Planning Ltd. All rights reserved. Privacy Policy | Disclaimer | Cookie Policy