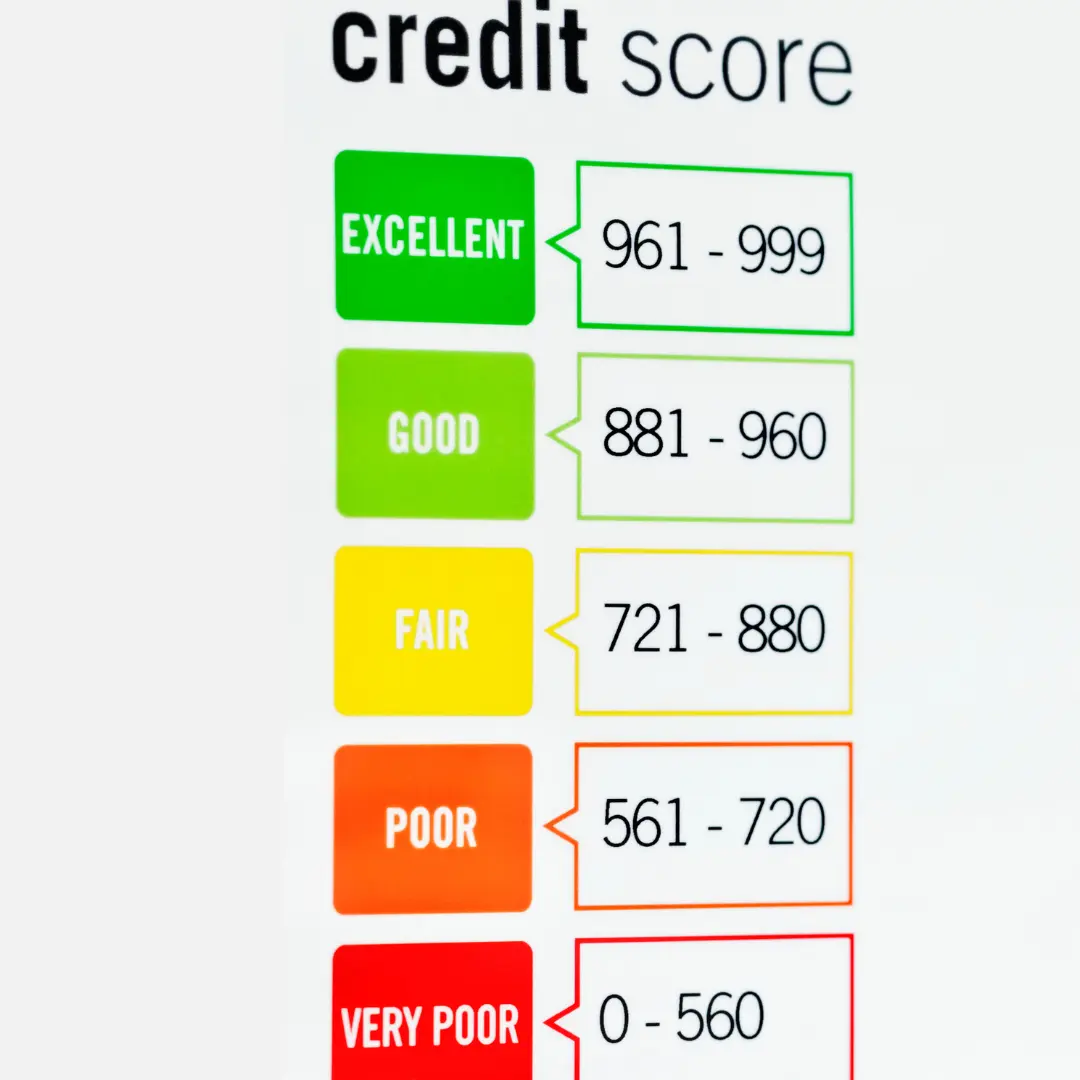

What counts as “bad credit”?

“Bad credit” is a broad term. Lenders usually care about the type of issue, the amount, and whether it’s recent or historic.

- Missed payments (especially within the last 12–24 months)

- Defaults (and whether they’re satisfied/settled)

- Mortgage arrears (history of missed/ late mortgage payments)

- CCJs (amount, date, satisfied vs unsatisfied)

- Arrangements such as DMP/IVA (and when they ended)

- High credit utilisation (maxed-out cards/limits)

How lenders assess remortgage applications with bad credit

Lenders typically look at your application as a full picture — not just the credit score number. The main themes are risk and stability.

- How long ago the issue happened

- Whether it’s resolved (settled/satisfied)

- Your loan-to-value (more equity often helps)

- Income stability and affordability

- Evidence you’re now managing credit well

This is why “whole-of-market” research matters: criteria varies a lot, and the right match can save time and stress.

What are my remortgage options?

Depending on your circumstances, your options usually fall into one of these routes:

1) Switch lender

If your credit issue is historic or mild, you may be able to remortgage normally — often with a slightly narrower pool of lenders.

2) Product transfer

If switching is tricky right now, moving to a new deal with your existing lender can be a sensible stop-gap while you rebuild your profile.

3) Specialist lenders

For more serious or recent credit issues, specialist lenders can be an option — usually with tighter terms and higher rates.

4) Wait + improve

Sometimes the best move is a short delay to improve your profile (and your choices) — especially if issues are very recent.

Could a product transfer be a better option?

A product transfer means you stay with your existing lender and switch to a new rate. It can be useful when your credit profile makes a new lender application more challenging.

- Usually less underwriting than a full remortgage

- Often quicker, with fewer documents

- Can reduce the risk of an unnecessary decline

How to improve your chances of remortgaging with bad credit

- Check your credit report (make sure info is accurate and up to date)

- Reduce utilisation (bringing card balances down can help quickly)

- Avoid new credit right before applying

- Keep accounts stable (regular payments, no bouncing DDs)

- Get documents ready so the application is clean and confident

If you’re unsure where you stand, we can sanity-check your position and suggest the most sensible route (switch / product transfer / wait and improve).

FAQs

Sometimes, yes. It depends on the date, amount, and whether it’s satisfied. Some mainstream lenders may decline, while specialist options may be available. We’d look at your wider picture before advising a route.

Potentially, but options can be limited while a plan is active. Some specialist lenders may offer options depending on how long the plan has been in place and your recent payment history.

Usually yes, at least initially. However, many clients remortgage again to a mainstream lender after rebuilding their credit over time.